VI: A Bill is a Bill

The beginning of 'Part Two' of the blog. On Hegel's use of bills of exchange as an example of value.

We are now in Part Two of the loosely structured arc of this blog. [And no, I do not know how many parts there will be.] Over the next several entries, we will be getting a better handle on the stakes of saying—as Hegel, Marx, and Thompson do—that ‘value’ is the term that marks the link between time and money as a specifically modern one.

The difference between this investigation into the stakes of the claim that time and money measure value and the investigation that drove Part One is that Part One was primarily concerned with the content of that statement—namely, with what the value concept actually refers to. Hence its focus on questions of form and substance, mediation and measure. Here, what we’re concerned with is the question of what motivates that statement and what that state implies or entails about the shape of our society—in other words: what critical leverage is the concept of value supposed to supply?

We will also need to get more specific about how it is that this idea might actually involve a tacit denial of the idea that money can meaningfully buy time. Part of what is at stake here is the question of what the difference really is—if any—between medieval and modern monetary orders. If we accept for the sake of argument that there is a substantial difference between the way medieval European societies related to money and the way our own societies do, and if we accept that ‘capitalism’ is more-or-less unavoidable as a name for our way of relating to money, then one way to phrase what these next few entries are concerned with is as follows:

First, what does an insistence on the centrality of value imply is distinctive about capitalism?

Second, is this really what is distinctive about capitalism after all?

To begin to answer these questions, we first have to understand what it might mean to insist that abstract and impersonal value is a formal and juridical principle specific to modern (i.e. bourgeois) civil society—what it might mean to say that ‘value’ is not the form in which things are forced to present themselves in every society there is or ever has been. In the Zusätz to the discussion of Abstract Right where he discusses money’s capacity to stand as a sign for value—the same one I quoted at length in my entry on the grammar of abstraction—Hegel offers two specific examples of value’s specificity, each of which encodes an important clue. Today we will be looking at only one of them; next time we will focus on the other.

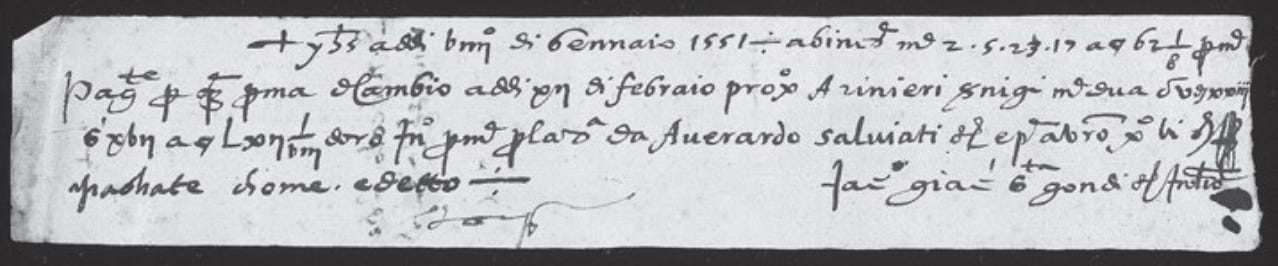

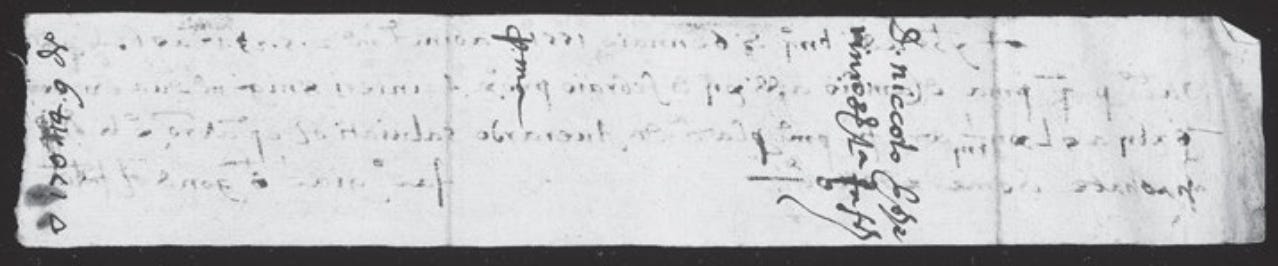

The first example Hegel offers to illustrate the impersonal character of value is the circulation of bills of exchange—informal financial instruments which first came into widespread use sometime around the twelfth or thirteenth centuries among the exchange bankers of the Italian city-states. Traditionally, a bill of exchange takes the form of a letter in which one party orders another party to pay a third party on their behalf. It is most often used as a way for a commercial exporter to demand payment for goods delivered to an importer who has purchased them on credit. Instead of moving hard cash over land and sea, a bill of exchange enables pairs of merchants transacting across the boundaries between distinct monetary jurisdictions to settle their accounts entirely on the books. To do so, they enlist the help of dealers who are willing to quote prices for foreign currency in domestic currency and vice versa.

Say, for instance, I am an exporter in Lyon who has sent a shipment of silk to an importer, Borgherini, in Florence. I receive notice that the goods have been delivered, and I know this means I am owed money. But unfortunately for me, this also means that the money I am owed is in Florence—not Lyon. I could, of course, send Borgherini a bill and order him to send me cash. But if I do this I will receive Florentine scudi, which are worth less in Lyon than they are in Florence; and in any case, coins are both risky and expensive to move. Alternately, I can go to the exchange fair and contract with a local exchange banker, Salviati. Salviati will give me local cash—Lyon marcs—and write up a cambium, or bill of exchange, on my behalf. He will then forward the bill to Florence, where I will draw on my account with Borgherini. Once it gets there, the bill will not order Borgherini to pay me, the drawer; it will order him to pay Salviati’s correspondent in Florence, Sernigi. Assuming Borgherini does not dispute the charge, he will have to pay Sernigi Florentine scudi at the end of the bill’s period of usance, anywhere from thirty days to three months. Once everyone has settled up, Borgherini has paid for the silk in his money and I have been paid for the silk in mine; meanwhile, Salviati and Sernigi, the corresponding bankers, have paid out marcs in Lyon and collected scudi in Florence. Salviati has an account with Sernigi that Sernigi will have to settle at a later date.

Hegel insists that a bill like the one delivered to Borgherini “does not represent its quality as paper, but is merely a sign representing another universal, namely value.” His choice to offer the bill as a stand-in for value, however, raises a deceptively simple question: value for whom? After all, a bill is just that: a bill. If I am presented with a bill, it does not mean I have money; it means I owe money. Today, one could be forgiven for confusion on this point. Recent historians of finance have often assumed that the medieval exchange by bills must have served as a disguised form of commercial credit. On the basis of this assumption, they have come up with increasingly tortured ways to misrepresent the web of relationships between the various parties involved. At the limit, some historians have even imagined that a bill represents a promise of payment in the hands of its recipient, essentially reversing the order of the transactions involved—all at the cost of making themselves unable to say why, exactly, the bills did not fall afoul of the ban on usury. To clear the air, we will eventually have to return to this issue and examine the transactions undergirding the exchange by bills in more detail—in particular, the process by which the dealers themselves make money on the exchange.1 But for now, what is important to note is that these specific confusions postdate the Philosophy of Right by more than a century. They do not explain what Hegel means when he tells us that a bill represents value in the hands of its bearer.

What Hegel likely has in mind is what bills of exchange became only after the usury prohibition had been lifted—namely, a negotiable instrument. Near the turn of the seventeenth century, the practice of endorsing and transferring discounted bills gained gradual acceptance, effectively enabling a bill issued by a drawer to behave as if it were a note issued by its drawee. A drawer, in other words—typically, the exporter who has sent a bill drawing on his balance with an importer—can sign the bill over to an intermediary who will be paid in place of the exporter’s representatives or his foreign business partners. This intermediary can again endorse the bill to someone else, and so on, down the line. In effect, the drawer of the bill, along with each subsequent intermediary, can choose to be paid sooner rather than later by passing the bill to someone else—generally, someone who will offer them less than the full value of the bill at maturity, but will pay today rather than tomorrow, next month, or next year.

The negotiable bill rose to prominence largely on the back of its central significance for one financial circuit in particular: the ‘triangular trade’ in slaves and associated securities between Liverpool, West Africa, and the West Indies. Representatives or ‘factors’ of Liverpool slaving companies operating in the West Indies would purchase bills drawn on London at a discount from the planters to whom they sold slaves. These planters, after all, were exporters themselves; they held outstanding balances with the London importers who had purchased their cotton and rum. Factors—essentially wholesalers in slaves—would turn these bills over to the captains of the slave ships in return for the slaves they were about to sell to the planters. The captains then sailed the bills to Liverpool, where they redeemed them for cash from the factor’s home office; the home office received cash for them at bill markets like those in nearby Lancashire, whose dealers redeemed them with the London importers against whom the bills had been drawn in the first place. Passed along in this way, negotiable bills could underwrite shipping ventures with extremely long time horizons, sometimes years between initiation and remission—ventures that had previously been impossible to finance without inviting crises of liquidity. This idiosyncratic use of the bills as a means of payment, known to its contemporaries as the ‘bills in the bottom’ system, turned out to be quite difficult for competitors to replicate with any long-term stability. As a result, it has often been offered as a key factor in the tendency for Liverpool-based firms to crowd out their competitors in the West Indian leg of the slave trade.

Negotiability makes it possible to convert a bill—a demand for payment—into something that can be handed over as a means of payment itself, enabling it to play a role not unlike a note or a check. But in order for a bill to plausibly represent value for its bearer, some fairly strict conditions have to be in place. The exporter’s demand for payment, for example, has to inspire enough confidence that it can be treated as if it already implied a promise to pay on the part of the importer to whom the demand is addressed.

Every bill exposes its signatories to a certain amount of counterparty risk. The drawee, after all, might repudiate the bill and claim that the drawer is attempting to charge them for goods they neither purchased nor received. Because of this, the chance that an importer might dispute the charge must be small enough that it is worth an exporter’s while to assume responsibility for it even before the bill has been formally accepted. This risk was assumed by every party who formed a link in the chain of endorsements. Throughout the seventeenth, eighteenth, and nineteenth centuries, commercial law in Europe and the Americas was fairly unanimous in its insistence that the liability assumed by an endorser of a negotiable bill was unlimited. If it turned out that someone had passed a bad bill, then each successive bearer was entitled demand the full value of the bill from the bearer who had sold it to them. In such an event, the Lancashire brokers, for instance, would have had to come after the Liverpool slaving firms for their money; the slaving firms would have had to come after the captains; the captains would have had to come after the factors, and so on, down the line. A remittance procedure like the ‘bills in the bottom’ system requires confidence that it is possible to price one’s exposure to the risk that some percentage of planters and factors are passing what amount to fraudulent checks, and that this price is low enough that it can be covered by the ‘haircut’ taken when a bill is purchased at its discount rate.

Bad bills are not the only potential source of counterparty risk in play. Even if a drawee does not dispute the legitimacy of the charge, they could still turn out to be insolvent or unable to pay when usance expires and the bill comes due. This too is a risk that must be able to be priced into the aggregate if discounted bills are to appear acceptable, even desirable, as a means of payment. The implicit promise of money represented by the bill—in reality, a promise that someone else has made a promise—must inspire enough confidence that it can circulate as if it were already money or near money itself. This kind of confidence does not come for free.

A system based on bills that pass through so many hands, over such long periods of usance, and across such enormous geographical distances presents a number serious problems for any attempt to settle and collect in the event that too many bills turn out to have been unpayable or issued in bad faith. In part, this why the ‘bills in the bottom’ model turned out to be so difficult to replicate. It depended heavily on the density of the personal and professional networks factors used to ensure that the planters were good for their promises. It also depended the sheer volume of the trade. In this way, the ‘bills in the bottom’ system was not entirely unlike the market in collateralized debt obligations (CDOs) whose collapse was at the heart of the 2008 global financial crisis; both relied on the idea that while the risks embedded in individual securities could never be reduced to zero, they could be packaged and priced in the aggregate. It must be emphasized, then, that the possibility of this procedure was not simply the inevitable result of the ‘deregulation’ represented by the lifting of the prohibition on usury and the legalization of negotiability for the bills. Negotiability had been slow to find acceptance and rarely extended to such extremes in large part because the dealers themselves found it too risky to be profitable. In order for bills to pass like notes or checks, new social, institutional, and legal infrastructure had to be put in place. As Hegel would put it, a bill can come to represent value only in the context of a highly specific Sittlitchkeit, or juridico-ethical form of life. And so the question becomes: what was the nature of this change?

Colin Drumm discusses a number of these issues here, and I owe quite a bit of my ability to cut through the tangle of scholarship on the bills both to his work on this issues and to the discussions that came out of the Mimbres School’s reading group on the book Private Money and Public Currencies by Marie-Thérèse Boyer-Xambeau, Ghislain Deleplace, and Lucien Gillard, which remains the banner theoretical and historical work on the mechanics of the early-modern market in bills of exchange.